Events

Upcoming events

Virtual Workshop : Last Mile Payments & Aid Distribution in the DRC

Members event

Crown Agents Bank in partnership with Paycode will be running an insightful virtual workshop on Last Mile Payments & Aid Distribution in Democratic Republic of Congo (DRC) on 16th May 2024. The workshop aims to provide practical assistance to field officers and regional staff involved in implementing programs with a last mile payment and aid delivery component.

Attendees will be able to...

CALP TAG (Technical Advisory Group) Meeting

Members event

The TAG helps shape and steer the CALP Network’s technical and policy priorities within the overall strategic vision for the network. All TAG Representatives are from CALP member organizations or are independent members of CALP. The TAG meets quarterly to: Review and provide feedback on key technical and policy products. Help define thematic priorities for the network, including defining...

Regional Cash Working Group – WCAF

Event

This is a Save the Date for the next Regional Cash Working Group meeting that will take place on Wednesday May 22nd, from 12pm to 2pm (GMT) face to face and online.

The meeting will have simultaneous interpretation in English and French.

The draft agenda for this meeting will be:

National CWGs round table (45 minutes).

Community approaches to emergency response through the Group Cash...

Global Cash Working Group – May meeting

Members event

You are invited to the next meeting of the Global CWG on Thursday, 23 May, from 1 - 230 pm UTC (9 am EST, 2 pm BST, 3 pm CEST, 4 pm EAT).

Please find the tentative agenda below and feel free to email to suggest additional agenda items:

1. Refreshing the Global CWG TOR

2. Update from the global Cash Advisory Group

3. Presentation and discussion of The Choice Model: User-Centred CVA...

Core CVA Skills for Programme Staff Training: St. Lucia

Training

Catholic Relief Services (CRS) EMPOWER (Empowering Partner Organization Working in Emergency Responses) project, Caritas Antilles, and the CALP Network are five days of in-person training for professionals based in the Eastern and Southern Caribbean. Objectives Understand how key norms, standards, and guidelines guide CVA. Understand how CVA should be integrated into the role of different...

Special Session: AIDONIC Humanitarian bulk disbursements Working Group

Event

Use this link to request a registration for CALP Network's Special Session with, AIDONIC and the Humanitarian digital bulk disbursements Working Group. Capacity is limited - event links will be shared 3-days before the Session.

Session timing, 6th June 2024 8am-9.30am US-EST

The Working Group is hosted by the CALP Network and supports humanitarian Cash and Voucher Assistance (CVA)...

Looking Back to Work Forward: CVA in the Americas

Event

Background Although humanitarian CVA is not new to the Americas, its use at scale and in various contexts throughout the region is a recent phenomenon. With at least five years of widespread humanitarian CVA in the Americas, there is an opportunity to review the maturity of the use of the tendencies, and where there could be more growth of CVA in the Americas. To address this opportunity,...

CALP Board Meeting

Members event

The CALP Board provides strategic leadership and operational oversight of CALP. It operates on the basis of the Operational Framework and Code of Conduct. The CALP Board meets a minimum of four times a year, online. For more information, go to the Board page.

Mongolia Cash Working Group Learning Event

Training

Please note that this is a six-day face-to face dovetailed event, which intends to gather those involved in CVA programming in Mongolia and are members of the Cash Working Group (CWG). It will take place in Ulaanbaatar, Mongolia. The deadline for registration/application is at 11:59pm, 28th April 2024, Mongolia time. With the intention to gather the learnings and reflection from the ongoing...

CALP TAG (Technical Advisory Group) Meeting

Members event

The TAG helps shape and steer the CALP Network’s technical and policy priorities within the overall strategic vision for the network. All TAG Representatives are from CALP member organizations or are independent members of CALP. The TAG meets quarterly to: Review and provide feedback on key technical and policy products. Help define thematic priorities for the network, including defining...

CALP Board Meeting

Members event

The CALP Board provides strategic leadership and operational oversight of CALP. It operates on the basis of the Operational Framework and Code of Conduct. The CALP Board meets a minimum of four times a year, online. For more information, go to the Board page.

CALP Online: Core CVA Skills for Programme Staff – Key Aid Consulting

Members training

CALP Board Meeting

Members event

The CALP Board provides strategic leadership and operational oversight of CALP. It operates on the basis of the Operational Framework and Code of Conduct. The CALP Board meets a minimum of four times a year, online. For more information, go to the Board page.

Past events

Filter by

1 – 20 of 291 results

Advocating for Cash and Voucher Assistance with Governments

Members event

Join the Cash Hub for our latest webinar: 'Advocating for Cash and Voucher Assistance with Governments'.

Monday 13th May 2024 at 14:00 CET (60mins, online)

Discover how advocacy and collaboration with governments are vital for leveraging Cash and Voucher Assistance (CVA) in humanitarian responses,...

Agility, Resilience through Local Capacity Investment in Humanitarian Action

Members event

This hybrid interactive panel session at the Humanitarian Networks and Partnerships Week (HNPW) spotlights speakers from Senegal, Ukraine, India, Tuerkiye from LNGOs, INGOs, discussing how humanitarian preparedness, learning from and investment in local capacity in community and staff skills enables...

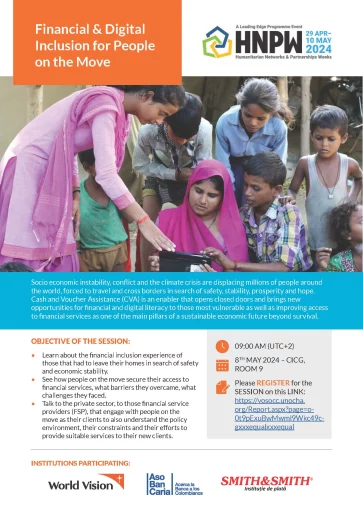

Financial and Digital Inclusion for People on the Move, Hybrid Panel Session HNPW

Members event

Socio economic instability, conflict and the climate crisis are displacing millions of people around the world, forced to travel and cross borders in search of safety, stability, prosperity and hope. Cash and Voucher Assistance (CVA) is an enabler that opens closed doors and brings new opportunities for...

Linking humanitarian assistance and social protection – common principles and country experiences

Members event

About the webinar: More and more people are living in contexts of protracted crises, driven by conflict, climate vulnerability and socio-economic fragility, requiring new ways of working together and stronger coherence between interventions across the HDP nexus. Linking HA and SP provides a clear...

Humanitarian Cash Response in Gaza – Sharing experiences and lessons learned

Event

This event will focus on the humanitarian cash response in Gaza, as well as the response in Palestine as a whole amidst the ongoing emergency. We will host the Cash Working Group coordinators where we aim to provide a platform for stakeholders to discuss the work of cash actors in Gaza, the achievements...

USA & Canada Community of Practice Meeting

Event

The overall objective of the meeting is to create a space for exchange for CVA actors working in the USA and Canada. Interested CVA professionals based in the USA and Canada are welcome to attend.

Special Session: Thunes Humanitarian payment solutions Working Group (closed)

Event

Session timing, 23rd April 2024 8-9.30 US-EST

The Working Group is hosted by the CALP Network and supports humanitarian Cash and Voucher Assistance (CVA) implementing organisations to leverage the latest digital payment infrastructure, to improve the quality, quantity and impact of support. It focuses...

Humanitarian Cash and Voucher Assistance in the USA: learning and sharing together

Event

Objective To provide a once off space that facilitates exchange and learning for the actors implementing humanitarian Cash and Voucher Assistance (CVA) in the United States. We aim to provide an environment to share knowledge, experiences, and best practices to enhance the effectiveness of their...

Report Launch and Panel Discussion: Achieving Resilience by Linking Humanitarian CVA to Social Protection in MENA

Event

Join as for a rich panel discussion on linking humanitarian CVA to social protection in MENA!

Please join us on April 18th 2024 from 15:00-16:30 Amman time to launch CALP's new report on the Feasibility of Achieving Resilience by linking vulnerable populations receiving humanitarian CVA to development...

CALP Online: Core CVA Skills for Programme Staff – Afghanistan

Training

Please note that this round of applications is for professionals based in Afghanistan only. Participation from women practitioners is highly encouraged.

Core CVA Skills for Programme Staff Training in Kyrgyzstan

Members training

Please note that this is a 5-day face-to face-course, which will be delivered in Bishkek, Kyrgyzstan on 15th – 19th April 2024. This training will be delivered in English with translation to Russian.

Lifeline at Risk: Supporting Markets through Cash in Sudan

Members event

Lifeline at Risk: Supporting Markets through Cash in Sudan

Nearly one year into the conflict that plunged Sudan into a humanitarian catastrophe, the international community is facing the humbling realization that the response has so far failed to match the severity and scale of people’s needs. In a...

CVA, Climate and Environment Community of Practice – Anticipatory Action and Cash

Event

Anticipatory Action and CVA: Understanding and Exploring Key Concepts, Issues, Approaches, and Perspectives. The webinar will be delivered at times friendly to the Americas and Asia Pacific regions.

Americas Regional Cash Working Group

Event

This is a Save the Date for the next Regional Cash Working Group meeting that will take place on Thursday, March 7th 2024, from 9 am to 11 am (Panamá local time) via online. The meeting will be conducted in Spanish with no translation: CALP strategy for 2024 (15 minutes) Presentation on the research...

Digital CVA reading group – Discussion of Brookings Institution Global fund paper

Event

This is an informal and private space for us to discuss two related papers:

- The call for a Global Fund for scaling digital cash transfers by Rory Stewart and Cina Lawson [Link - https://www.brookings.edu/wp-content/uploads/2023/12/2023-Room-1-Concept-Note.pdf]

- The paper referenced in this: Updating...

MENA Membership Engagement Event

Event

Online- March 6th, 2024, 11:00-13:30 Amman time

Regional Cash Working Group – WCAF

Event

This is a Save the Date for the next Regional Cash Working Group meeting that will take place on Wednesday March 06TH, 2024 from 9am to 11am (GMT) face to face and on line The meeting will have simultaneous interpretation in English and French. The agenda for this meeting will be: National CWGs round...

CALP Board Meeting

Members event

NGO Policy Dialogue Roundtable

Members event

ICVA and CALP would like to invite NGOs to a one-hour roundtable discussion for NGOs on 29th February at 9am UTC as part of a BHA and CALP convened CVA Policy Dialogue process. Please register here.

As part of the process, constituency roundtables have been organized e.g., among local organizations,...

South Sudan Joint Markets Monitoring Initiative (JMMI) Workshop

Members event

South Sudan Cash Working Group in collaboration with REACH and the CALP Network East and Southern Africa Regional Office wishes to extend an invitation to all CWG Members collecting JMMI data for the JMMI Workshop on Enhancing Market Monitoring in South Sudan. The virtual workshop is scheduled for...